Table of Contents

Note: This report is a product of, and completely owned by, Galaxy Research. It was originally published on Galaxy’s official website here:

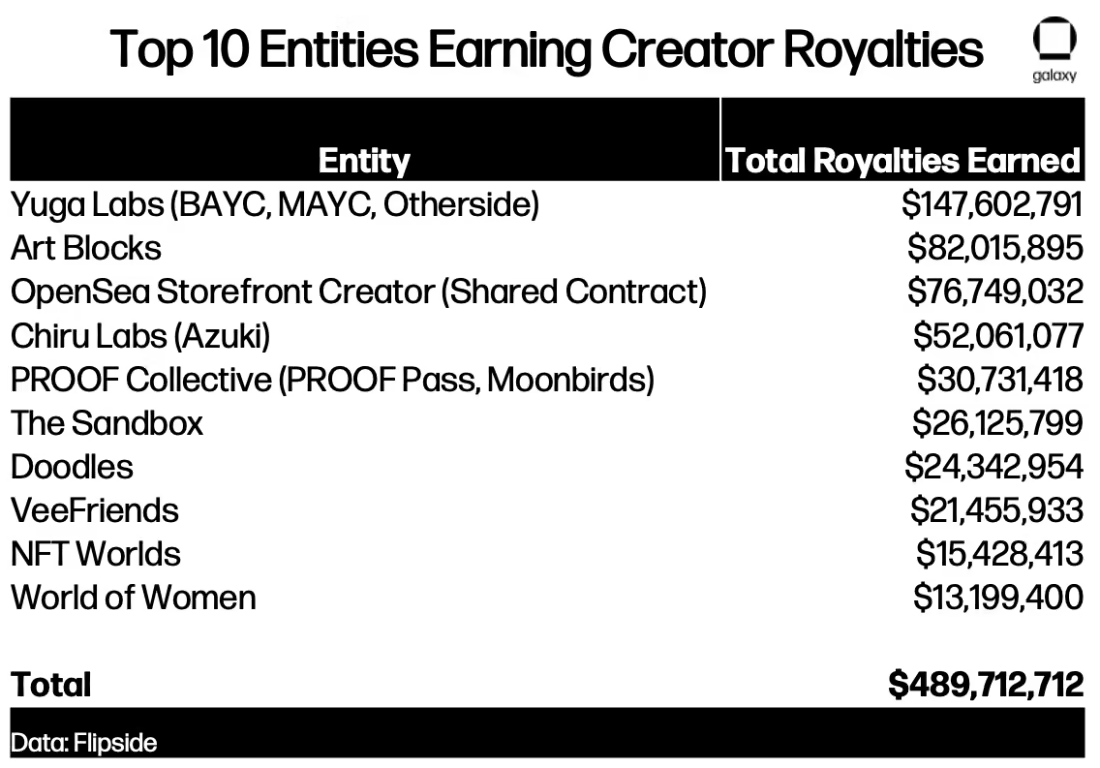

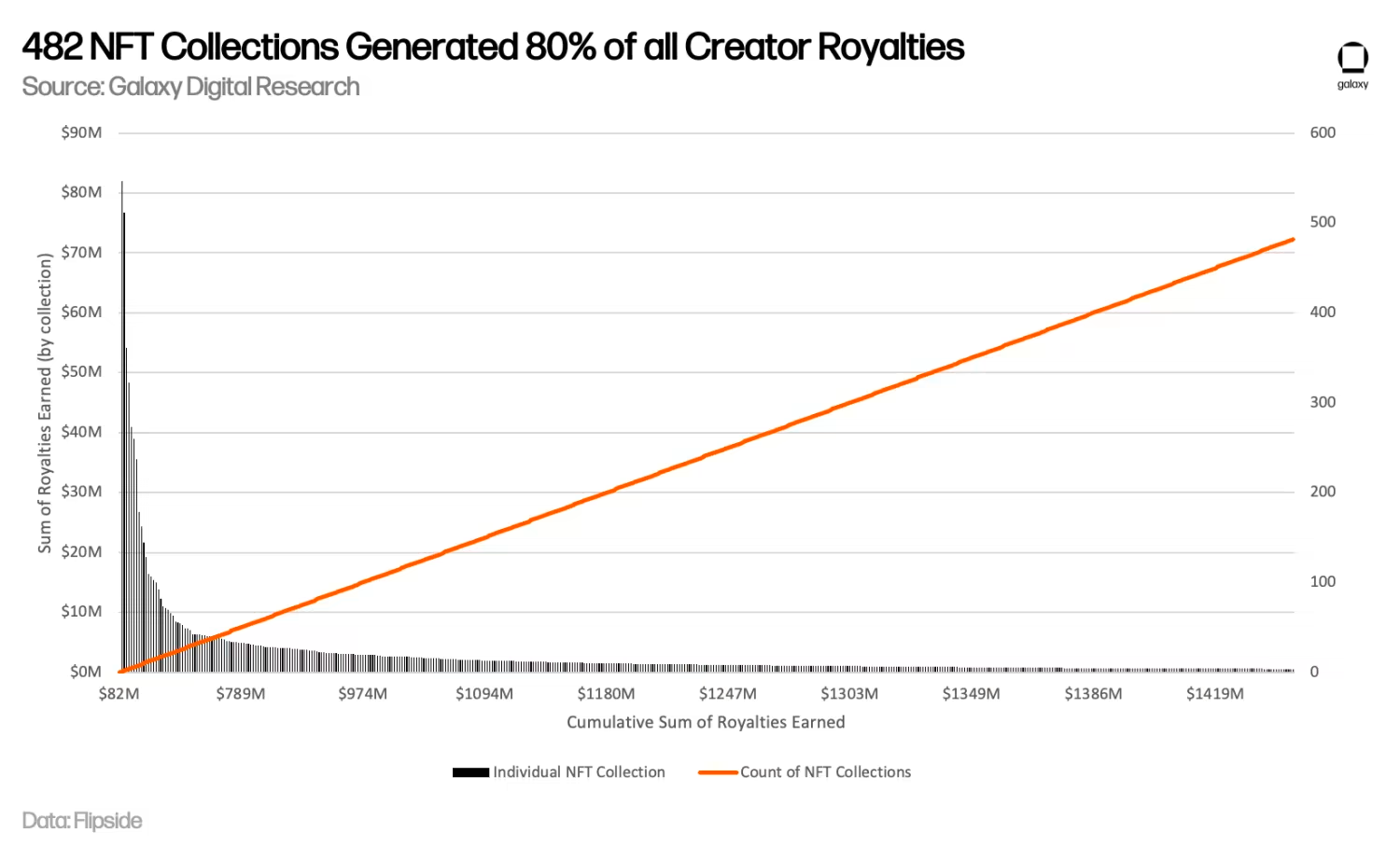

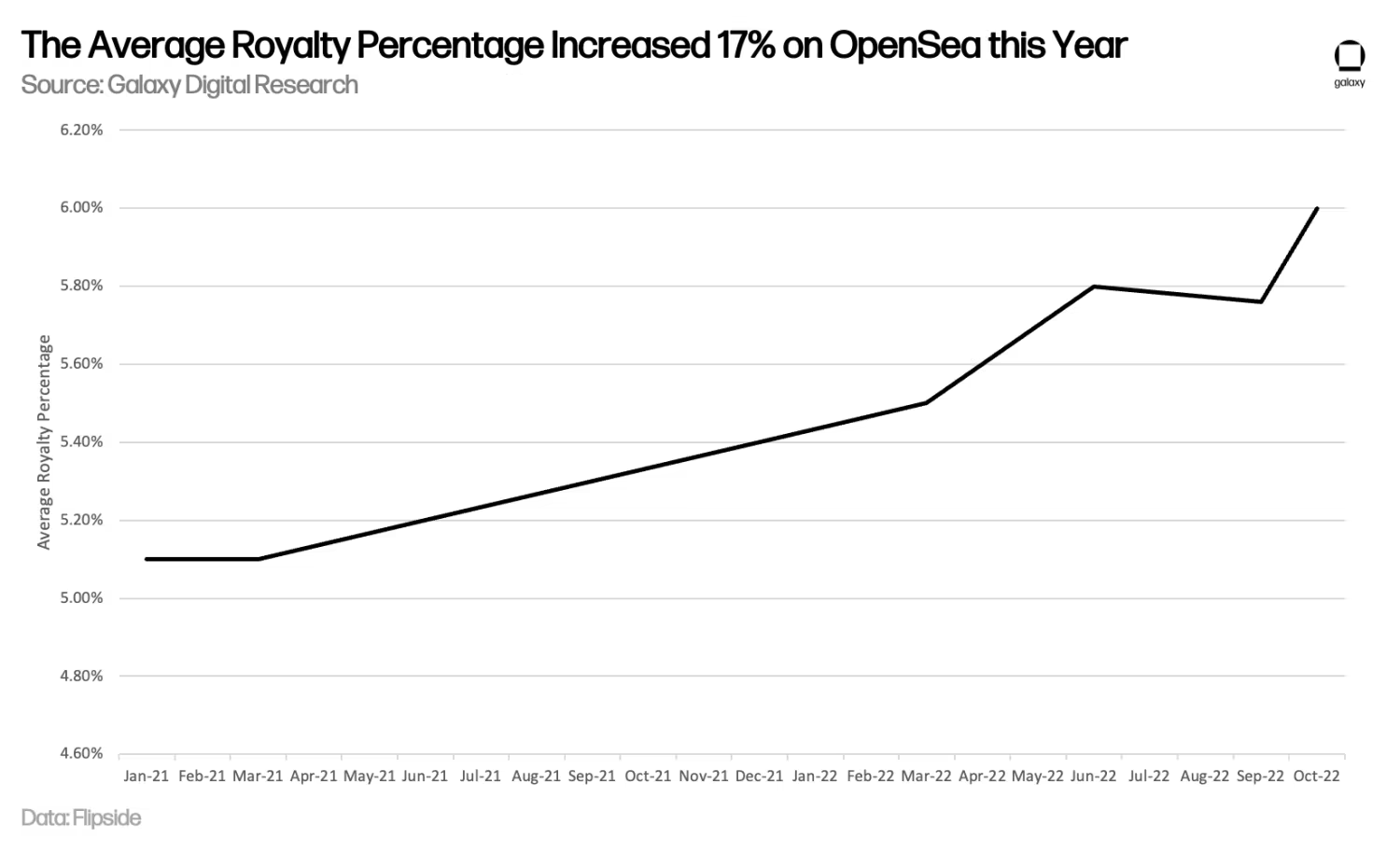

Over $1.8bn worth of royalties have been paid out to creators of Ethereum-based NFT collections. In addition, the average royalty percentage paid out to creators on OpenSea, the platform that has paid out the most royalties to creators by far, has doubled from 3% to 6% over the past year. Major brands in NFTs, across both legacy players and crypto-native organizations, have raked in hundreds of millions of dollars in income from royalties generated on secondary sales. In fact, just 10 entities accounted of 27% of all royalties earned and 482 NFT collections accounted for 80% of all royalties earned thus far. Yet recent pushback against the royalty model in the broader crypto community is poised to threaten what was once posited as a core value proposition of NFTs. The reality is that royalties aren’t a primitive that inherits the same on-chain permanence that has been taken for granted in the crypto space.

Our Methodology

All of our data, including our top-line $1.8bn in royalties earned and entity/collection-level metrics, were calculated using Flipside’s data tables. The specific data source we are referencing in these calculations is Flipside’s ethereum.core.ez_nft_sales SQL database table, where we are filtering on records where the creator_fee_usd parameter is greater than 0. While no calculation for royalties will be perfect, we are comfortable with Flipside’s methodology in ingesting, transforming, cleaning, and storing Ethereum NFT trading data. We then aggregated the collection-level NFT royalties from Flipside by-hand into known entities for our Top 10 Entities Earning Creator Royalties graphic.

How Royalties Work Today

Until recently, NFT royalties have been an opaque aspect of NFT trading. First, sellers pay for royalties, not buyers (similar to the commission model of real estate transactions). Second, royalties are not actually programmed at the token/smart-contract level. Concretely, smart contract transfer mechanisms such as Ethereum's transferFrom() function cannot be relied upon to calculate royalty payments owed since these functions also are used when collectors transfer NFTs between their own wallets. The only way an NFT royalty could be programmed into a smart contract is if the program somehow knew precisely when an owner is transferring an asset between his/her own wallet or selling an NFT to a buyer. This is not possible to do without introducing some degree of either 1.) centralization in the form of an intermediary that keeps tracks of wallets and ownership of assets or 2.) undermining the self-sovereignty of digital assets by allowing intermediaries to revoke features of user-custodied assets based on their behavior. Furthermore, even if programmed into the contracts, despite the bad UX of forcing users to pay even when they are only shuffling their own self-custody, the NFTs could be moved into a wrapper contract and then the wrapped versions could trade without triggering additional royalties.

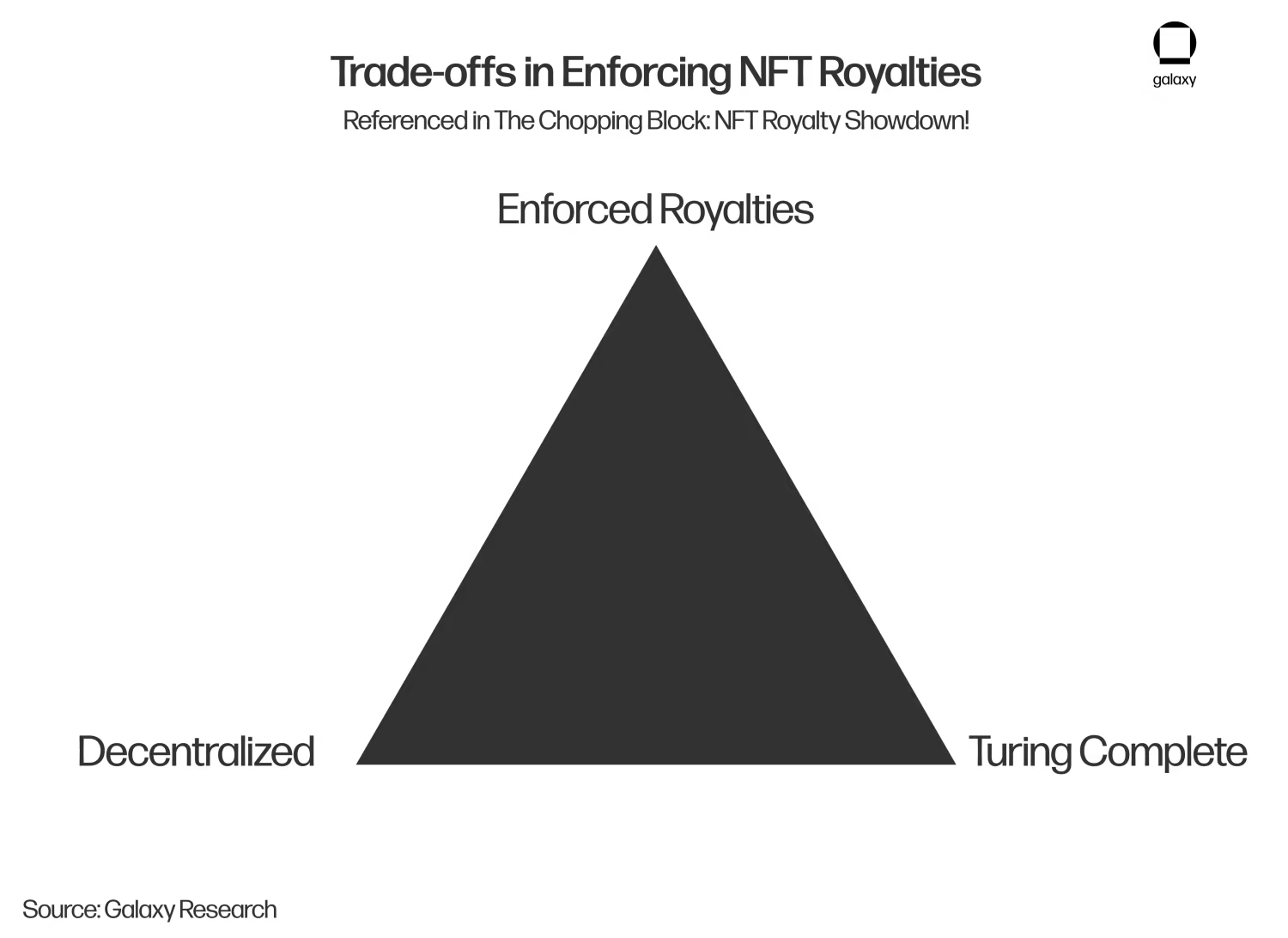

In a recent episode of The Chopping Block, Haseeb Qureshi of Dragonfly and Zhuoxun Yin of Magic Eden discussed a trilemma between successful enforcement of royalties, decentralization, and Turing completeness. Successfully optimizing for all three of these properties is currently infeasible, which is the key reason why NFT royalties are not yet implemented at the token/smart contract level.

Due to the technical difficulties in enforcing royalties at the smart contract level, they are instead enforced by NFT marketplaces. In other words, royalties are socially enforced by norms, and marketplaces are effectively choosing to support the ongoing funding of creators by collecting and disbursing royalties on their behalf (similar to tipping). Thus, the majority of NFT marketplaces have implemented bespoke royalty payment solutions in order to entice creators with the promise of ongoing revenue streams. This was important in the early days of NFTs as protocols needed to appease both sides of the marketplace, creators and collectors. Now that the NFT space has matured substantially in the last 2 years, marketplaces have adapted accordingly. As stated above, some marketplaces like SudoSwap have eliminated royalty payments entirely to attract as much liquidity as possible.

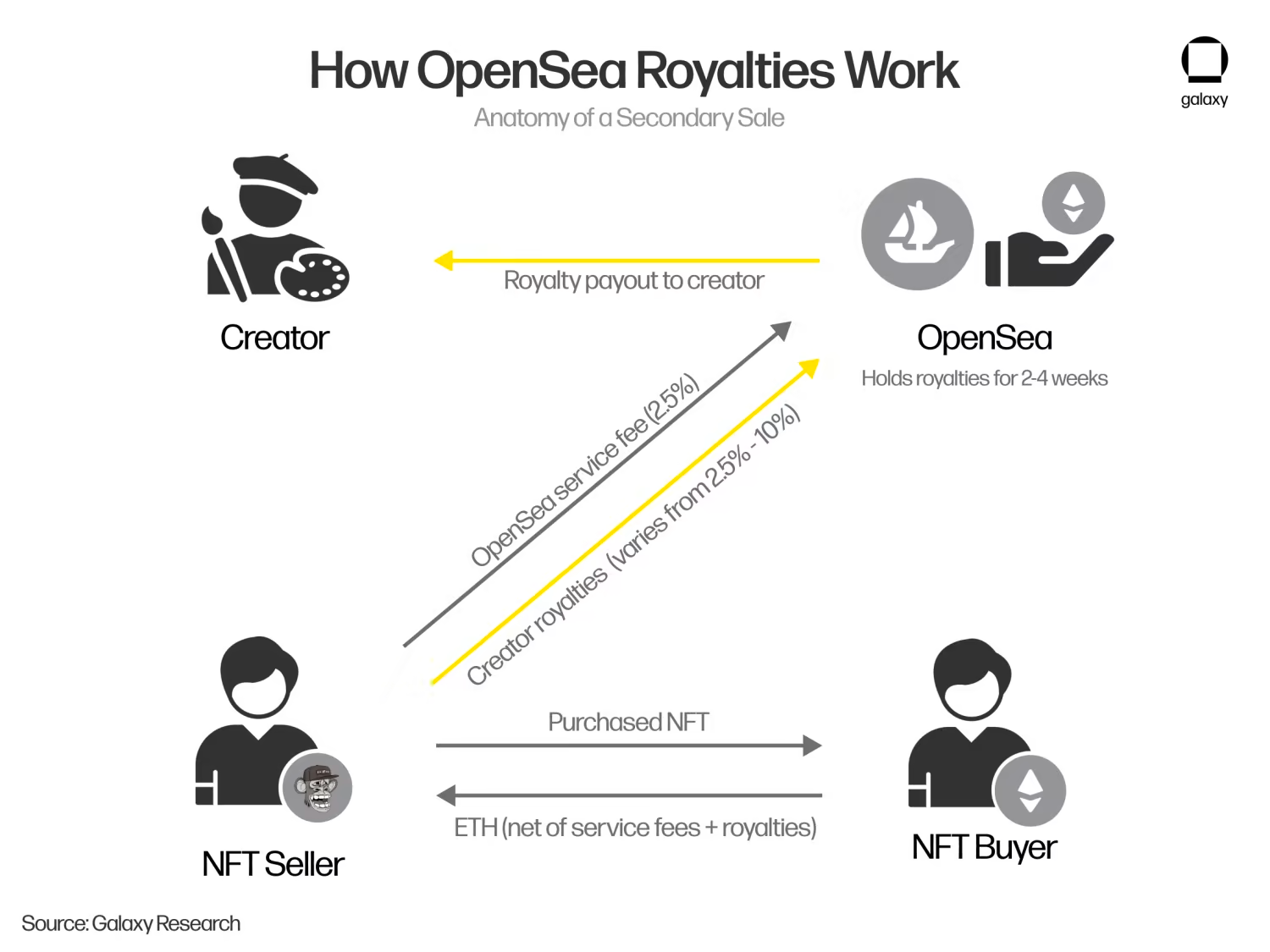

OpenSea currently accounts for 80%+ of NFT marketplace volume, and their method for royalty distribution is the most common framework implemented by marketplaces today. In this framework, creator royalties are defined at the collection level and must be set up within OpenSea’s collection-level settings by the collection owner. During this process, the creator will also associate a wallet address with the collection which will be designated to receive accrued royalties from OpenSea at regular intervals (usually every couple of weeks). Royalties generally range from 2.5% up to a limit of 10% of the final sale price. The seller always pays both the royalties and the trading fee collected by OpenSea on each trade. These fees are typically extrapolated away, with buyers simply paying the amount quoted by OpenSea as the NFT’s price (or the winning auction bid) plus gas fees.

Introduction

NFTs revolutionized the economic relationship between creators and consumers by giving rise to the concept of creator royalties on secondary sales. Until NFT royalties came into the picture, artists traditionally only made money from primary sales of their works. That restrictive economic paradigm ensures that artists, especially those whose work may be seen as too revolutionary for their time, are unable to grow their revenue stream as their work gains recognition. The logical extreme of this restrictive economic model, from a historical perspective, may be best represented by renowned artist Vincent Van Gogh. Van Gogh struggled with poverty throughout his life and only sold one painting, The Red Vineyard, for 400 francs in Belgium several months before his death. While he was never famous during his lifetime, Van Gogh would eventually emerge as one of the most famous painters in history, generating over $670mn of secondary sales volume after he died. It’s not hard to imagine a universe where Van Gogh was able to capture a royalty from his secondary sales, channeling this ongoing revenue stream revenue towards a posthumous cause of his choosing (such as arts education initiatives).

On the one hand, NFT royalties are an avenue through which creators can generate additional income from the ongoing success of their work. This business model has been particularly advantageous for digital artists and musicians, who have historically struggled to recoup profits from traditional channels of distribution such as galleries and record labels. On the other hand, there is a growing belief among some in the crypto community that NFTs should be owned entirely by their buyers, and that royalty payments to creators are unfair and extractive. Crucially, NFT royalties are currently enforced by the marketplaces themselves, not hard-coded into the issuing smart contracts. The decentralized nature of the crypto space has birthed a variety of NFT marketplace structures which posit royalty-free NFT trading as a core value proposition.

Lately, the ongoing question over NFT royalty enforcement at the marketplace level has prompted a tidal wave of changes across dominant players in the NFT ecosystem. The DeGods ecosystem recently removed royalties from all their affiliated NFT collections (DeGods, y00ts). This move happened despite the fact that DeGods’ founder, Frank, has defended royalties multiple times on Twitter, and he still believes that royalties are the best incentive-alignment mechanism between NFT collection operators and holders. Some exchanges, albeit lesser ones, have also moved to alter royalty payments (or remove them), such as x2y2, although the biggest, OpenSea, has not. Additionally, Solana NFT marketplace juggernaut Magic Eden made the controversial shift to make all royalties on their platform completely optional. Magic Eden’s latest move in eradicating royalties is especially noteworthy considering that they anncounced MetaShield, a controversial tool designed to improve enforcement of royalties, in September 2022.

There are compelling arguments on both sides of this debate. While royalties have proven to be a lucrative revenue stream for collection owners, they are unenforceable at the smart contract level as demonstrated by the rise of royalty-free marketplaces. The NFT community appears to be split on the ideology underpinning royalties, with some positioning royalties as beneficial for an NFT ecosystem’s health and others lamenting royalties as exploitative and unnecessary. Given the massive stakes at play in terms of potentially lost revenue streams, this issue has the potential to leave long-lasting impacts on the NFT space for years to come. In this report, we will examine the issue of NFT royalties from multiple perspectives and suggest how we see this key issue will materialize.

A Brief History of NFT Royalties

NFT royalties are a relatively new phenomenon when compared to the age of the NFT space itself. CryptoPunks, considered to be the godfather of the 10,000 item generative PFPs, never instituted royalties when they debuted in 2017. The official CryptoPunks exchange, the only marketplace where Punks are traded, still do not enforce any royalties on secondary sales. Larva Labs, the creator of CryptoPunks, opted for an alternative business model where they chose to instead hold 1,000 Punks on their balance sheet, selling these Punks off sporadically to generate revenue.

Yuga Labs then stormed onto the NFT scene with their Bored Ape Yacht Club collection in mid-2021 and, in the process, demonstrated the economic allure of a royalty-driven business model. While BAYC only generated $2.2mn in primary sales when they launched in May 2021, the collection has since earned Yuga Labs $54m in secondary sales revenue by way of BAYC’s 2.5% royalty on every transaction. Yuga Labs has earned a staggering ~$140m in royalties from all their collections to-date. Other NFT projects took note of Yuga’s success and instituted 2.5% royalties as standard practice. As the NFT market continued to heat up throughout the second half of 2021, the industry standard of 2.5% soon jumped up to 5% (on the backs of collections like Azuki, Doodles, CloneX, and Moonbirds). Yuga Labs capitalized on this trend towards higher royalties when they launched their Otherdeeds collection with a 5% royalty and switched Meebits from a 0% royalty to a 5% royalty. Otherdeeds alone has yielded the company $44m in secondary sales revenue since its launch in April 2022.

Royalty fees have only increased since the mania of the Otherside land sale. Goblintown, for instance, debuted with a completely free-to-mint collection that capitalized on a well-architected viral meme campaign on Twitter. Behind the veil of an “anti-Discord, anti-Roadmap, anti-utility” ethos, Goblintowns quietly programmed a 7.5% royalty (which was very high for the time) on all secondary sales. This ultimately netted the team ~$7m in revenue for a collection that was ultimately nothing more than a meme. The highest royalty fees might be metaverse collection NFT Worlds. Their 9.5% royalty, one of the highest for a prominent collection, has netted the team $15m despite NFT Worlds land trading 94% down from all-time highs. The platform is also home to a paltry 235 daily active users. Given the poor performance of the collection and weak user growth, some community members have become upset with the project’s founders continuing to receive royalties.

As the broader bear market has punished NFTs in both price and volume, the users are more price-sensitive than ever before. The market has also started to push back against collections earning ongoing revenue, by way of royalties, despite not delivering on their ambitious visions. This brewing resentment towards royalties, along with some recent innovations in marketplace structure, have ultimately ignited a surge of activity on royalty-free NFT marketplaces.

How Did We Get Here?

SudoSwap (which we originally covered in our NFTs & DeFi report) was the genesis of the anti-royalty movement in the NFT space. SudoSwap, which launched in July 2022, leverages an AMM model for NFT trading (similar to how Uniswap works for fungible tokens). Their goal with the AMM model is to improve liquidity and market making for NFTs while minimizing fees. Not only does SudoSwap take a comparatively low trading fee of 0.5% (compared to 2.5% for OpenSea), they also do not support the enforcement of any NFT royalties for collections themselves. While SudoSwap’s model works best for floor NFTs, their core value proposition has proven to be very popular with sellers who seek to enhance their margin wherever possible. Instead of losing as much as 12.5% to royalties and platform fees, sellers are instead guaranteed to pay a maximum of only 0.5% on every sale.

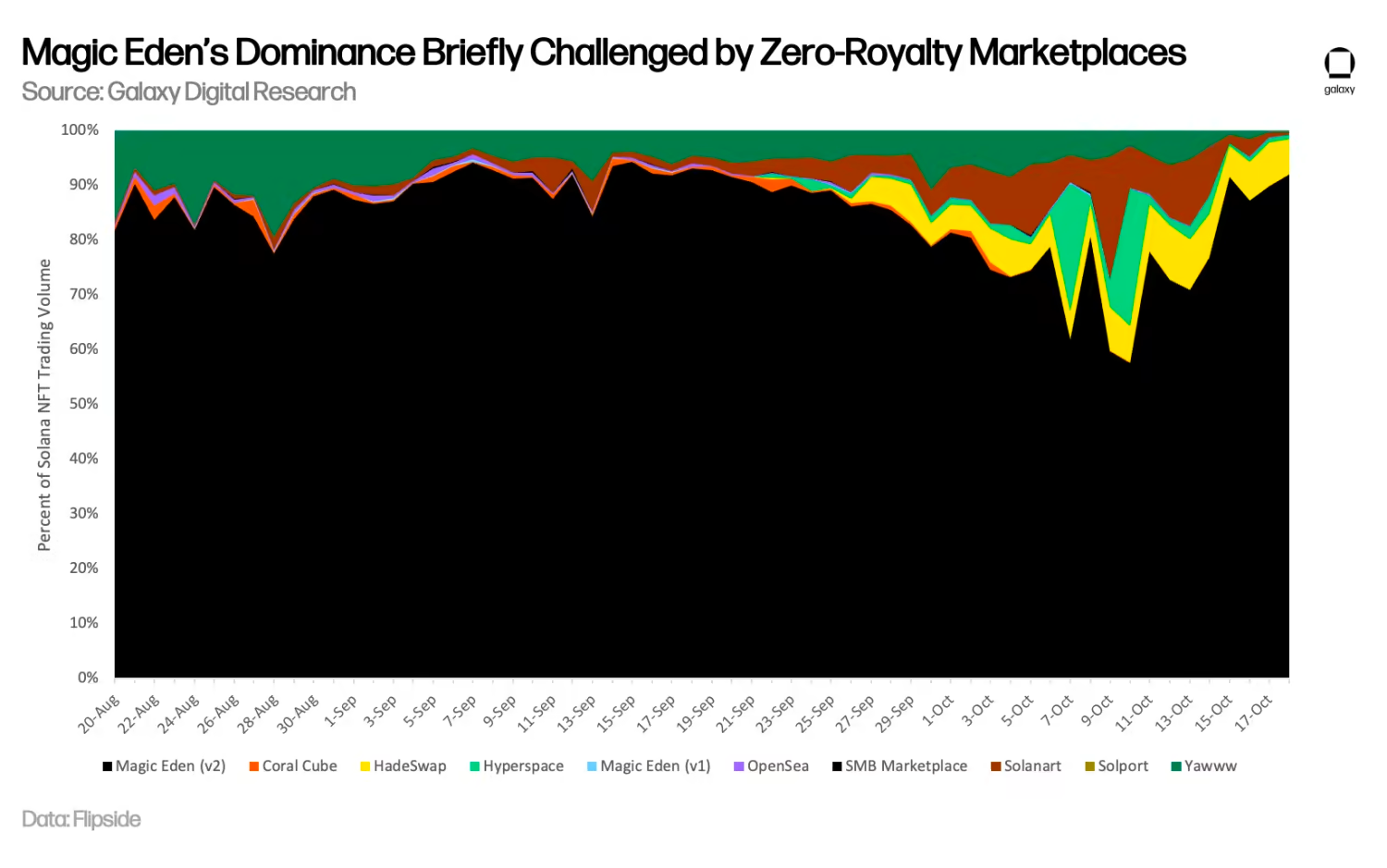

Once SudoSwap started to gain popularity as a preferred destination for selling NFTs, Gem took notice. Gem, which was acquired by OpenSea last April, is an NFT marketplace aggregator that helps users sweep floor NFTs with the lowest price possible across exchanges. Naturally, this meant that Gem started including SudoSwap in its list of aggregators. This small move prompted the broader NFT space to interpret Gem’s integration with SudoSwap as an endorsement of sorts from OpenSea. Soon after, another NFT marketplace, x2y2, followed suit and made it optional for buyers and sellers to pay royalties. At approximately the same time that x2y2’s eliminated royalties on the Ethereum side of NFTs, Yawww made an announcement on the Solana side of NFTs that largely mirrored x2y2’s announcement in making royalties optional. After Yawww nixed royalties on their platform, HadeSwap coincidentally launched later in the summer, mirroring SudoSwap’s approach in building a royalty-free, AMM model for trading Solana NFTs. By September, it appeared that the royalty-free movement, which appears to have initially started with Ethereum NFTs, took Solana NFTs by storm.

Magic Eden, which has historically commanded ~90% market share of the Solana NFT marketplace volume, saw its dominance challenged by the rise of royalty-free alternatives like Yawww and Hadeswap. According to data compiled by Tiexo, Magic Eden’s market share started to drop precipitously in October, falling from ~90% down to as low as ~60% over the span of a few weeks. In response, Magic Eden announced they would make royalties optional on their platform in order to level the playing field with these fast-rising challengers. Since the announcement, Magic Eden’s market share has since climbed back up to their prior level of ~90%.

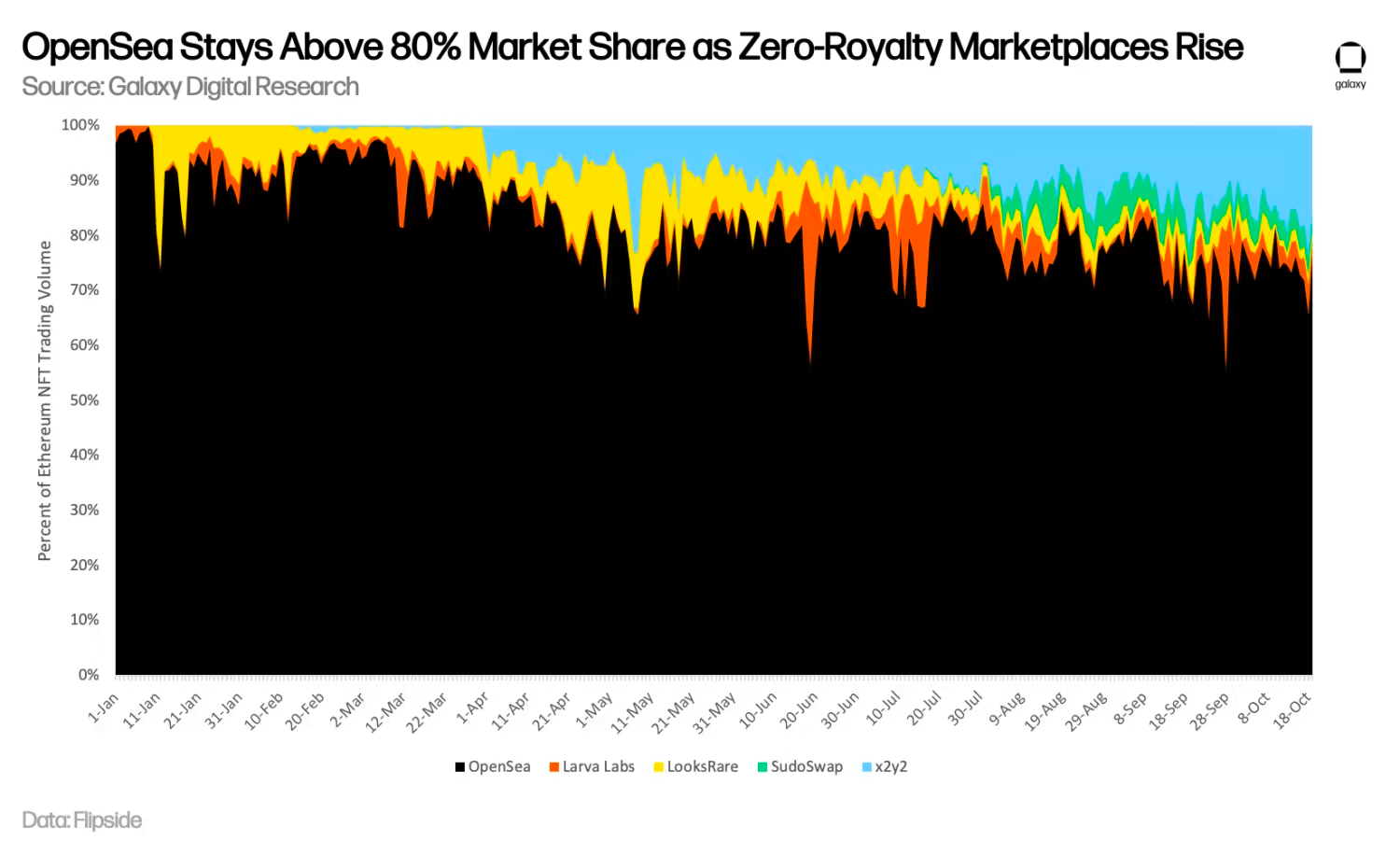

It's interesting to note that the Solana NFT ecosystem has been more sensitive to this ongoing royalty debate than the Ethereum NFT ecosystem, as evidenced by the massive shift in market share away from Magic Eden before their move to eliminate royalties, while the magnitude of OpenSea’s market share loss to zero-royalty marketplaces was much smaller. One possible explanation is the more mercenary nature of Solana NFT traders who tend to be flippers cognizant of their margins rather than longer term holders and retail users. On the Ethereum side, there are far more high USD value collections, like Fidenzas and Punks, which attract a class of buyer that is perhaps more interested in signaling status and storing value in these rare collectibles than flipping them for quick profit. In other words, these high-net-worth users are not sweating the royalty fee enacted on each sale.

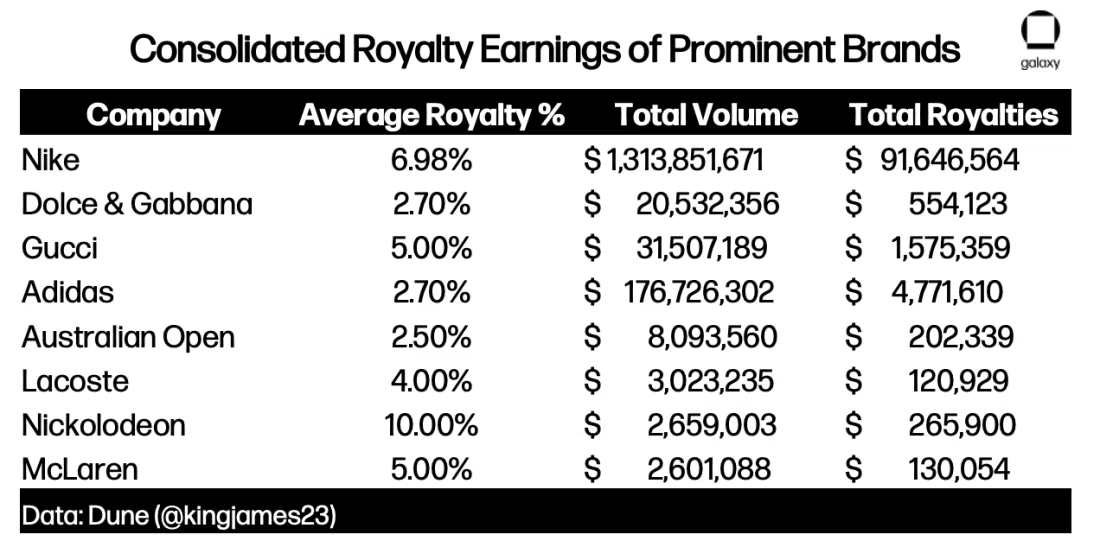

Tyler Hobbs, creator the Fidenza and QQL generative art collections, has supported the claim that the behavior of Ethereum’s NFT community is inherently different from Solana’s NFT community. Hobbs stated, “The serious artists and serious collectors tend to be in Ethereum, rather than on Solana. It's a much better test of those systems, and I think creators will put up much more of a fight when it comes to Ethereum.” So far, Hobbs’ perspective that Ethereum’s NFT community will fight hard for preserving royalty rights appears to be correct as OpenSea, which enforces royalties, remains the dominant platform. Apart from individual creators, major brands like Nike, Gucci, and Adidas also stand to lose tens of millions of dollars in potential revenue if royalties are no longer enforced. We expect these massive legacy institutions and marquee creators to fight hard to preserve their royalty-driven revenue streams from Ethereum-based NFT collections.

The Debate

In the ongoing royalty wars, two leading schools of thought have emerged. Those in favor of royalties point to the potential for creators to earn more money over time as their projects become more popular. This is because projects often start with low primary sales, but gain popularity in the months following release. DeGods and BAYC are two clear examples of NFT collections with small primary sale numbers before catapulting into the upper echelons of their respective ecosystems in less than a year. Proponents of royalties worry that normalizing the their removal will return the NFT space to the dark ages of traditional creator incentive structures, as Van Gogh experienced.

On the other hand, opponents of royalties claim that enforcement mechanisms are not possible on-chain without severe trade-offs that negate many of the advantages of permissionless blockchains in the first place. Even Solana creator and esteemed engineer Anatoly Yakovenko admitted that the only feasible way to enforce royalties at the token-level is to reimagine what the concept of ownership looks like. In his view, ownership of the NFT could be split between the user and a creator-defined smart contract. This would allow the creator’s smart contract to implement royalties and grant them the power to strip away the user’s NFT in the event he/she fails adhere to the royalty parameters set forth in the token’s smart contract. This construct has clear pitfalls for the concept of self-sovereignty that many believe are anathema to the entire purpose of NFTs. Royalty opponents also argue that collectors in the NFT space are incredibly price-sensitive and will increasingly favor marketplaces that offer the lowest fees. In their view, fighting for royalties is impractical, and the inevitable shift away from royalties means that creators would be better served developing more sustainable business models.

Several major NFT players have offered solutions to address and/or augment royalty enforcement.

Initial Noteworthy Responses:

Tyler Hobbs’ QQL mint card project is the first major NFT project to prevent transacting on 0% royalty fee marketplaces at the smart-contract level. This function is performed through a blacklist filter contract, which checks if the msg.sender (the person trying to buy the NFT) is on a blocked list of users before allowing them to complete their purchase. If the msg.sender recipient detects a blacklisted user, the transaction will automatically fail. Hobbs added existing anti-royalty marketplaces to the blacklist. The QQL project has brought attention to the idea that if NFT marketplaces have the privilege to decide whether to follow the royalty system, then NFT creators should also have the privilege of deciding which marketplaces can sell their artwork.

Although Magic Eden has since reversed course, they initially attempted to combat the 0% royalty movement with a tool called MetaShield. This new optional feature allows creators to track and identify Solana native NFTs listed on 0% royalty platforms such as Yawww. Through MetaShield, the creators of these projects can deliberately modify the metadata for the NFTs that are attempting to bypass royalty payments. Not only can the MetaShield tool blur or erase NFT images, but it also creates an accountability system for buyers. If a buyer purchases an NFT that has bypassed royalties and is shielded, the buyer will rack up a debt for the unpaid royalty. The debt must be paid to "unshield" the NFT's image. Though Magic Eden received backlash for this buyer accountability system, the company clarified that this was put in place to incentivize recognition of creator rights.

Manifold, one of the most noteworthy NFT smart-contract developers and tooling providers, has presented an eye-opening solution to the royalty distribution crisis. Manifold has collaborated with OpenSea, Rarible, Nifty Gateway and SuperRare to launch an on-chain contract that makes it easy for marketplaces to adhere to a project’s desired royalty. The key problem Manifold is solving is that creators must manually update their desired royalty percentages within each marketplace that their NFT trades on. This is problematic because any new exchange that emerges will not explicitly know what the preferred royalty preferences for an existing NFT collection is. Additionally, creators would also be burdened with manually updated their preferred royalties at each exchange if their royalty preferences change. Manifold is standardizing this burdensome process by creating tooling to let creators update their preferences in one place, on-chain. Manifold refers to this as a royalty registry contract, and it makes it possible for smart contracts that did not previously support on-chain royalties to easily add them. While royalty registries do not necessarily aid in enforcement of royalties, they do make it much easier for developers to adhere to existing royalty preferences for creators in an on-chain manner. This approach is very similar to what was originally proposed in EIP-2981: The NFT Royalty Standard.

Outlook, Conclusion, & Potential Solutions

As NFTs continue to evolve, the future of royalties hangs in the balance. While the numbers suggest that Ethereum NFTs still have a strong contingent of users willing to pay royalties, the royalty-free marketplaces have shown impressive growth in a short period of time. One thing is certain: the future of NFT creator income hangs in the balance as industry stakeholders weigh the pros and cons of this contentious issue. Only time will tell if creators continue to reap benefits from secondary sales, or if they will lose out on potential income in favor of a “pure” ownership model. As this dynamic market continues to grow and mature, it will be interesting to watch how stakeholders carefully consider potential long-term solutions to this ongoing battle. Some potential solutions include:

Buyer’s Premium: In Beeple’s view, switching the onus of royalty payment from sellers to buyers makes a ton of sense. Since buyers are seeking to enter an NFT ecosystem, they are likely more willing to pay royalties since they are also likely to be leveraging some utility associated with the NFT (such as accessing a Discord, staking for rewards, or playing a game). In all these use-cases, royalty payments can be programmatically checked before the program grants the user access. On the other hand, sellers, since they are exiting a collection, are likely much less apt to want to pay an additional fee on their way out of an NFT collection. Thus, it’s not surprising that sellers have been more mercenary in nature when it comes to finding the best possible execution price for their NFTs. This dynamic is exacerbated by NFT flippers who simply seek to enter and exit NFT positions for the sole purpose of making a profit.

Vertical Integration of Marketplaces: When Crypto Punks debuted in 2017, they could only be bought or sold on Larva Labs' marketplace. By controlling the marketplace, Larva Labs was able to enforce its own royalty preferences (which has always been 0%). Today, both Yuga Labs and RTFKT are in the process of building their own marketplaces. This trend towards vertical integration draws many parallels to trends in ecommerce over the last decade with the rise of direct-to-consumer. The analogy here is that Amazon is like OpenSea, where distribution is maximized and profit margin is minimized. Companies that own their own storefronts on Shopify get to keep more of their margin. While it is unlikely that vertically integrated marketplaces will occupy the majority of NFT trading market share, this trend will likely ensure some degree of royalties for collections will always exist (similar to what we’ve seen with the rise of direct-to-consumer).

Alternate Revenue Streams: In a scenario where royalties are no longer guaranteed, some collections may be pressured to introduce subscription-based business models to maintain their repeatable income. Other collections will likely be pressured to monetize the collection’s IP with merchandise sales or business deals outside of crypto (in-person events, restaurants, TV shows, games, movies, etc.). While this is likely good for the NFT space in the long run, as it can force an ecosystem’s hand in delivering on a long-term strategy, we would not be surprised to see many failed attempts on this front. The key question we ask when it comes to generating alternate revenue streams is, what is the purpose of an NFT collection? If NFT collections are supposed to be like businesses, then this approach makes logical sense. However, those who view collections as decentralized communities that ought not to be profit-motivated may be disillusioned by this trend.

Higher Mint Prices: The simplest antidote to reduced revenue from royalties is to increase revenue generated from primary sales. It’s possible that this approach will only work for established NFT ecosystems with a pedigree of success. However, we do see a world where mint prices are expected to rise over time (just as we saw royalties creep up from 2.5% to 7.5% over the past year). This trend towards higher mints may also lead to an increase in scams, however, due to the misalignment of incentives. As new projects raise more money upfront, they may be less tempted to deliver continuous value over the long run.

Regressive Royalty System: Initially proposed by jota.sol, this approach draws similarities to regressive tax systems that have been proposed throughout history. In this system, as the amount subject to taxation increases, the amount subject to taxation decreases. In the case of NFTs, the more that a given NFT is worth, the lower the royalty percentage would be levied upon sale. The economic theory underpinning this approach is referred to as the Laffer Curve, which posits that logical extremes in taxation both yield sub-optimal outcomes in terms of revenue generation. Said differently, there is likely an optimal royalty percentage along the Laffer Curve that most traders are willing to pay, and this percentage is >0%.

Enforcing Off-Chain Utility: This is similar to what Tyler Hobbs and MetaShield have already attempted, but it’s focused entirely on off-chain use-cases. The core idea here is that many users purchase NFTs to access a resource that lives off-chain (such as a game, staking platform, Discord server, etc.), this approach would simply gate-keep access to that resource based on whether the NFT owner paid a royalty. We are already seeing this implemented in NFT Discord servers where roles are granted based on past royalty payments. These enforcement mechanisms typically work by checking if an NFT was purchased on a royalty-free exchange, such as x2y2. By publicly ostracizing those who leverage royalty-free exchanges, it is possible that buyers migrate back to exchanges that implement royalties in the hopes of preserving the utility of their NFT.

Galaxy Legal Disclosure

Legal Disclosure:

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice or is an endorsement of any of the stablecoins mentioned herein. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital may have owned or may own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. This document provides links to other Websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider’s website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email contact@galaxydigital.io. ©Copyright Galaxy Digital Holdings LP 2022. All rights reserved.

.png)

Written by